CBIC has issued circular no. 105/2019 for Clarification on various doubts related to the treatment of secondary or post-sales discounts under GST.

In most of the cases of supplier and distributor channel, there are post sales discounts which are passed through the Credit notes. Taxability of discounts has always been under scanner. CBIC has grilled further in the issue and clarified following:

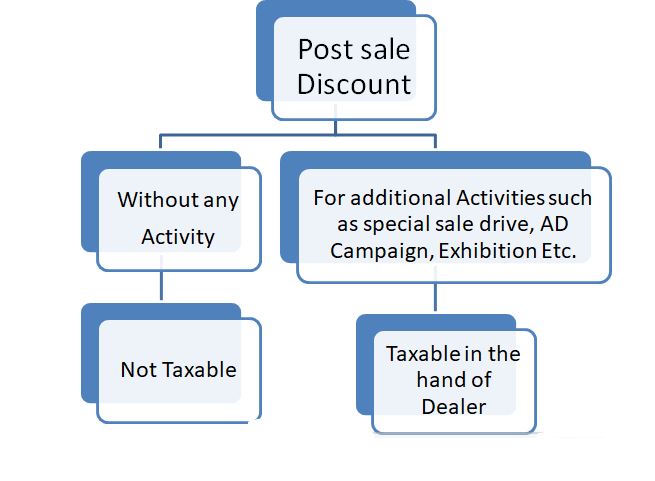

1. The post-sale discount has been bifurcated into two categories.

a. Post sales discount without any activity on the part of dealer: Not taxable

b. Post sales discount for activities such as Special Sales drive, AD Campaign, Exhibition - Taxable in the hands of the dealer.

It is further clarified that in case of discount being non taxable, The dealer would not be required to reverse the credit.

No comments:

Post a Comment